India Passenger Vehicle Sales FY2025: Fuelwise Breakdown

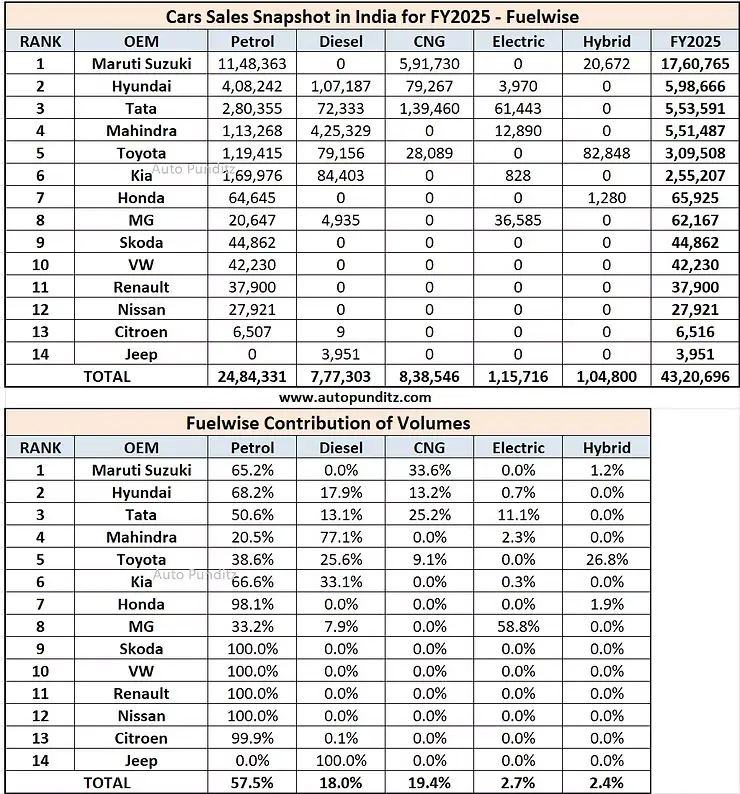

India’s passenger vehicle market recorded sales of around 43.2 lakh units in FY2025. This short report presents a fuel-wise view of these volumes to outline how different powertrains contributed to overall market performance during the year.

Petrol-powered vehicles continued to form the backbone of the Indian car market, accounting for close to three-fifths of total passenger vehicle sales. Petrol remained the primary choice across mass-market segments due to wide model availability and established ownership economics. While growth in petrol volumes has stabilised, its dominance remained unchanged through FY2025.

CNG emerged as a strong secondary fuel choice, contributing nearly one-fifth of total sales. Volumes were largely driven by manufacturers offering factory-fitted CNG options across high-volume models. Rising fuel prices and improved refuelling infrastructure supported steady adoption, especially in urban and semi-urban markets.

Diesel vehicles accounted for under one-fifth of passenger vehicle sales. Although diesel volumes continued to decline at an industry level, demand remained concentrated in SUV-focused portfolios where higher torque and long-distance usage remain key factors.

Electrified powertrains continued to grow from a low base. Electric vehicles accounted for under 3 percent of total sales, with volumes led by a limited number of manufacturers with established EV line-ups. Hybrid vehicles formed a similar-sized share, with sales concentrated among brands offering strong-hybrid technology.

Overall, FY2025 highlighted a diversifying fuel mix in India’s passenger vehicle market. Petrol retained its leadership position, CNG strengthened its role as a cost-efficient alternative, diesel remained relevant in specific segments, and electrified powertrains continued gradual expansion.

Data scope: Domestic passenger vehicle sales in India for FY2025. Figures are rounded and exclude exports and commercial vehicles.